Find a Lawyer

Book an appointment with us, or search the directory to find the right lawyer for you directly through the app.

Find out more

Legacy: Putting the Family First

This comprehensive guide is designed to help you navigate the intricate landscape of family business and private wealth in the Middle East, where family businesses constitute approximately 60% of GDP and employ 80% of the workforce in the GCC, offering unparalleled opportunities for wealth creation and preservation.

Packed with insights, strategies, and expert advice from our talented lawyers, Legacy provides tailored solutions to the unique challenges of asset protection, succession planning, and dispute resolution in this dynamic region.Read the publication and equip yourself with the knowledge and tools necessary to thrive, whether you’re a seasoned investor, a family business owner, part of the next generation, or a newcomer exploring opportunities in the region.

Read Now

A complete spectrum of legal services across jurisdictions in the Middle East & North Africa.

Closing Time! What to Expect at a Ship Sale & Purchase Closing Meeting

Omar N. Omar - Partner, Head of Transport & Insurance - Insurance / Shipping, Aviation & Logistics

James Newdigate - Senior Associate

Gabriel Yuen - Associate, Transport, Trade & Logistics

Ship sale and purchase transactions typically consist of several stages. A rough outline of stages may include:

- preliminary negotiations;

- inspection of the vessel and due diligence;

- signing of a Memorandum of Agreement (‘MOA’);

- preparation of documents and vessel for delivery; and

- closing.

Here the authors consider the final stage: closing. This stage concludes the sale and purchase of a ship and generally takes place after several weeks of preliminary actions. It is, in essence, where the ship (and relevant documents) are delivered against payment of the purchase price. This seemingly straightforward exchange does, however, involve numerous requirements and customs unique to shipping.

Legal and documentary requirements for closing need to carefully accommodate practical elements. Our aim in this article is to outline what parties may expect on closing day.

![]()

Where does the Closing Meeting Take Place?

Closing meetings may take a variety of forms. Here we outline a typical arrangement whilst acknowledging there are many possible variants. The structure is premised on the elected MOA being a Norwegian Saleform 2012 (‘NSF 2012’), arguably the most widely used MOA for ship sale and purchases.

Typically, there will be two simultaneous meetings on closing day. One meeting will take place ‘ashore’. This may be at the offices of one of the parties, their legal advisors, or even appointed escrow agents. This meeting leads the closing. The second meeting will take place ‘aboard’ (i.e. aboard the subject vessel).

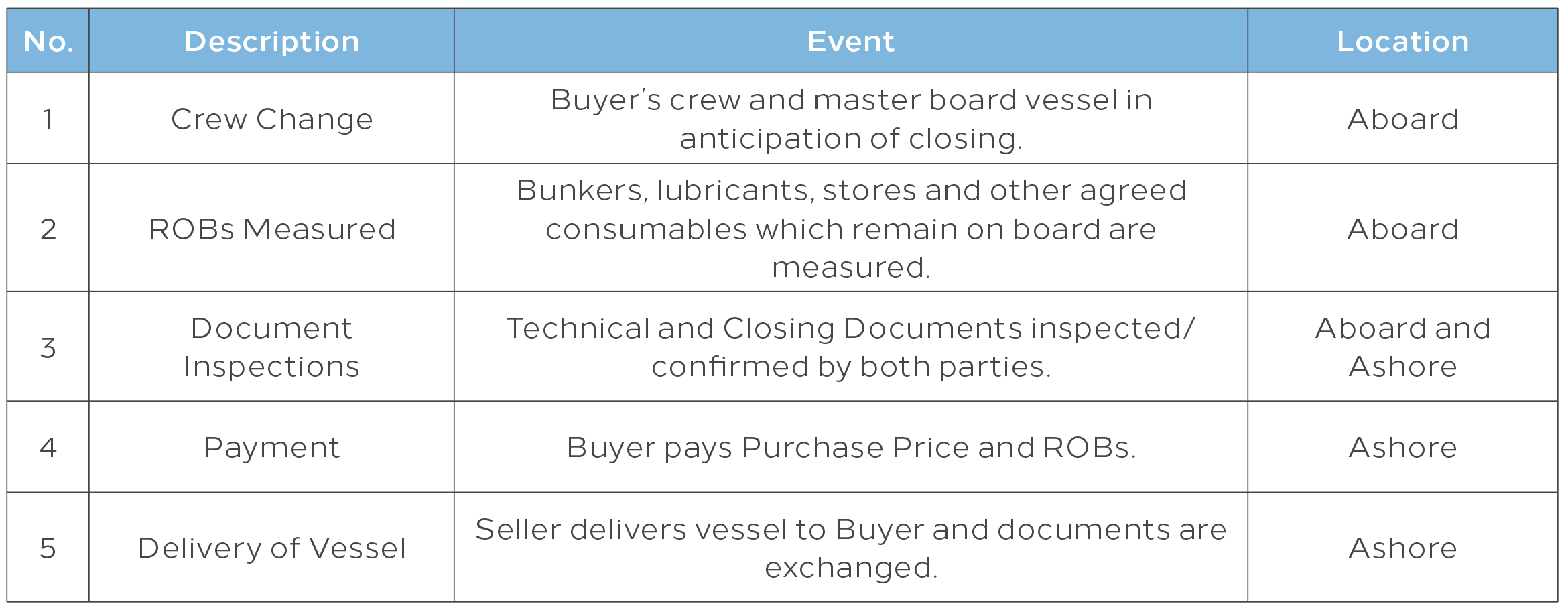

Roadmap of Events at Closing

There are a variety of parties which may be involved in a closing, each with its particular part to play. To aid an efficient closing, parties would do well to circulate a Closing Memorandum ahead of time. This document should detail who is required to do what, when. It should also provide an outline of all parties, the particular individuals required to be present on the day, and their direct contact numbers. A typical transaction may see the following parties involved at closing, whether required at one of the physical meetings, or on stand-by remotely:

- buyer and seller (with respective legal counsels);

- escrow agents;

- crews (led by masters);

- managers (technical, crew and commercial);

- flag state representatives;

- bank representatives (where subject to debt finance);

- sale and purchase brokers;

- insurance brokers/representatives; and

- ship agents

Assuming that the buyer and seller have jointly appointed an escrow agent to receive and release the purchase price (i.e. the deposit and balance) and payment for bunkers and lubricants remaining on board (‘ROBs’), a typical order of events at closing may be as follows (some actions occurring simultaneously):

Document Inspections

Documents inspected at closing are generally not documents the parties are considering for the first time. At closing, parties are normally only confirming that the agreed forms of documents are now present, in original and signed, if required.

There are typically two categories of documents in a ship sale and purchase: Closing Documents and Technical Documents.

(i) Closing Documents

These documents are normally listed in the body of the MOA (Clause 8 in the NSF 2012). These are key documents required for closing, some of which will only be signed and dated at the closing meetings. Examples of documents in this category are: the Bill of Sale; Powers of Attorney; Corporate Authorities; Certificate of Ownership and Encumbrances; and Certificate of Class.

(ii) Technical Documents

Generally, Technical Documents are documents required for the maintenance and operation of the vessel. Industry practice dictates the types of documents typically found in this category. The list of agreed technical documents is often annexed to the MOA.

Technical Documents are normally standard form and required by international conventions, for example: certificates pertaining to safety; pollution; communications; and insurance. Technical Documents are generally voluminous, and parties normally rely on appointed technical managers to consider the documents before closing to confirm they are in order, or advise of any deficiencies.

Many Technical Documents are kept aboard the vessel. This is a legal requirement for certain documents. At closing, parties will not normally inspect technical documents comprehensively, as this is done before closing. The exercise at closing is normally to confirm that the agreed documents are there and ready for delivery.

Crew Change

As previously noted, the legal and documentary requirements for closing need to complement practical considerations. This is especially true when considering command and control of the subject vessel. The incoming crew, led by their master, should be kept fully apprised of progress of the meeting ashore. Parties should be mindful that, at the moment the vessel is delivered, the new owner’s master is required to take command of the vessel and assume all associated responsibilities, legal and otherwise.

It is advisable to have direct communication between the two meetings. Practically, this means a speakerphone from boardroom to bridge, ensuring maximum transparency so as to avoid any mis-communications. Masters should record in the deck log, in real time, the exact time and place of physical delivery and change of command.

Bunkers and Lubricants Remaining On-board

Normally on the morning of closing the parties will agree the quantities of ROBs. Practically, this requires measurements of the bunkers, lubricants, stores, supplies and any other consumables subject to sale and separate payment. Parties may engage a third party to confirm these measurements, or simply arrange for the buyer’s and seller’s respective masters to agree figures, and advise the meeting ashore.

Payment

The buyer usually pays three sums at closing:

- deposit for the purchase price of the ship (‘Deposit’);

- balance of the purchase price (‘Balance’); and

- payment for ROBs.

Parties often appoint an escrow agent to receive and release all three sums. This is only one option for payment, with several alternatives. Should an escrow agent be appointed on this basis, by closing, all three sums should have been deposited into its bank account.

In instances where the escrow agent is facilitating the ROB payment, a buyer may pre-position an excess of funds with the agent, with any surplus returned to the buyer after the agreed amount has been transferred to the seller.

Delivery of the Ship against Payment

A closing meeting culminates with the signing of two critical documents: the Release Instructions to the escrow agent; and the Protocol of Delivery and Acceptance (‘PODA’). The former transfers the money, and the latter the ship.

At delivery, the vessel should be legally and physically ready for delivery, and this may be declared through a Notice of Readiness from the seller. Readiness in this instance also assumes the vessel is at the agreed location for delivery and in a satisfactory condition (e.g. in the same condition as per last inspection, fair wear and tear excepted). The seller will also generally warrant the vessel is delivered free of charters, encumbrances, mortgages and maritime liens, and indemnify the buyer accordingly.

Once the parties are satisfied that all documents are in order, and the vessel is ready, delivery against payment is the final step. The buyer will effect payment, normally through the provision of irrevocable release instructions to the escrow agents. Once the escrow agents acknowledge receipt, the parties may jointly sign the PODA which (legally) evidences delivery of the vessel. Here the time, date and vessel’s location at delivery are all noted – such details also being entered by the master in the vessel’s deck log.

Closing Remarks

Each closing is different. There are numerous moving parts and, inevitably, unexpected issues will arise. Parties should allocate sufficient time to close, be prepared to co-operate to overcome obstacles, and thoroughly plan beforehand.

Al Tamimi & Company’s Transport & Insurance team regularly advises on ship sale & purchases. For further information please contact Omar Omar (o.omar@tamimi.com), James Newdigate (j.newdigate@tamimi.com) or Gabriel Yuen at (g.yuen@tamimi.com).

Spread the news

Spread the news

Stay updated

To learn more about our services and get the latest legal insights from across the Middle East and North Africa region, click on the link below.